The pending implementation of the Department of Labor’s (DOL) new “fiduciary rule” is poised to dramatically change how retirement investments are managed. With this momentous change, the wealth management industry continues to rapidly shift to a fiduciary, fee-based model. Of course, not every advisor currently affiliated with an independent broker dealer (IBD) should start their own registered investment adviser (RIA) firm, but increasingly it is an option that all advisors currently with an IBD should evaluate. This is the first post in our two part series exploring the economic considerations of an advisor comparing the independent RIA model to affiliating as a representative of an independent broker dealer.

Level of Assets Required to Start and Operate an Independent RIA Firm

Many in the industry assume that firms need a significant amount of assets under management (AUM) in order to prosper. However, the industry stats paint a much different picture. According to Meridian-IQ, of the 2,159 new firms created in 2014, only 635 of those shops had an AUM figure greater than $50 million. Thus, over 70% of new RIA firms which are created start with less than $50 million in AUM. Furthermore, most advisors do not realize that the median AUM of the over 32,000 RIA firms currently registered is less than $20 million according to the latest publicly-available statistics.*

At RIA in a Box®, we continue to see an increasing number of small advisory firms thriving as more advisors seek to act as a fiduciary in every interaction with their clients. This is largely due to the rapid evolution of the ecosystem supporting independent RIA firms. From the registration process and onward, firms like ours along with a number of custodians, technology vendors, and others allow even the smallest of investment advisory firms to operate with incredible efficiency at an affordable cost. Compliance is a serious consideration for any new RIA firm, but again, firms like ours have experience helping thousands of fellow investment advisers implement comprehensive, yet efficient compliance programs with the benefits of the latest technology. The compliance program an independent RIA implements also correlates directly to their specific business and activity as opposed to the broader measures the advisor may need to adhere to under a corporate RIA regime.

For years, many independent broker dealers have stated that advisors need to have over $100 million in AUM in order to profitably operate an independent RIA firm. We respectfully disagree with these assumptions and believe the economic models below more than support our views. While there is no question that larger RIA firms benefit from increasing scale, even the smallest of investment advisory firms can operate quite profitability in today’s world of rapidly declining operational costs. In making any sound business decision, it is prudent to evaluate the numbers and facts as opposed to conforming to the general rhetoric that smaller advisory firms cannot survive or fictitious AUM requirements.

Understanding Independent Broker Dealer Payout Rates

Traditionally, independent broker dealers market payout rates in the range of 75-95% of annual advisor revenue production. However, as many independent broker deal representatives understand first-hand, such gross payout rates often do not fully reflect all expenses. Such additional expenses often include:

- Technology: These fees vary widely across the independent broker dealer industry and are often charged as a bundle or a la carte. These fees can be a profit center rather than a simple cost pass through for the broker dealer. In general, technology costs are at least a few hundred dollars per month for the average affiliated advisor.

- Administrative: Some independent broker dealers charge additional basis points in regards to the administration of fee-based accounts or third-party money managers. Others charge additional fees to advisors related to providing errors and omissions insurance or Security and Investor Protection (SIPC) coverage.

- Compliance: Some firms charge advisors additional fees related to compliance especially in regards to the supervision of outside business activity related to the advisor operating their own independent RIA firm. In addition, a number of firms also charge advisor registration and filing fees. Moreover, the complexity of meeting Financial Industry Regulatory Authority (FINRA) regulations often adds opportunity cost and cash outlays for advisor reps.

- Ticket charges: Compared to the traditional, self-clearing discount broker dealers that offer traditional custody and brokerage services to RIA firms, the ticket charges at independent broker dealers can be significantly higher. With limited or no ability to select an alternative broker to transact with, this can result in higher cost not just for the advisor, but for the advisor’s clients as well.

- Liability Insurance: Errors and omissions insurance provided by independent broker dealers is often marked up through a third-party intermediary. The advisor may also have to subscribe to an insurance policy that has associated underwriting risks built in because the advisor is operating within a heightened risk pool alongside all of the firm’s other advisors that conduct various types of securities business.

Of course, an advisor affiliated with an independent broker dealer is also generally responsible for covering all overheard expenses which may include:

- Staff salaries

- Office rent

- Office technology

- Marketing

The key economic differences for an advisor when affiliated with an independent broker dealer versus operating exclusively as an independent registered investment adviser firm are:

- Gross Payout Rate: When an advisor operates under their own RIA firm, the gross payout rate for revenue generated by the advisor is 100% compared to a gross payout rate that varies widely in the independent broker dealer industry.

- Direct technology, compliance, insurance, and other costs: Under a traditional independent broker dealer model, technology, compliance, insurance, and other services are provided directly by the independent broker dealer who then charges the affiliated advisor fees related to those services. As the owner of an independent RIA firm, the advisor makes such purchases directly with the appropriate service providers. While it can vary depending on the advisor’s size and business model, these direct purchases are generally comparable under both models. In addition, an advisor often has access to a much larger array of service providers at varying price points once operating an independent RIA.

- Ticket charges: When working with a traditional RIA custodian as an independent RIA firm, the advisor will be able to choose one or multiple custodians which offer the best capabilities to the advisor and their clients. Given the competitive nature of the custody industry, custodians’ ticket charges tend to be quite competitive and favorable when compared to many independent broker dealers that may mark-up such ticket charges.

Many RIA Firms Succeed Today with Less Than $25 Million in Assets Under Management

There is also a lot of misinformation that has been published in regards to the compliance and regulatory expenses for independent RIA firms. The fact is the vast majority of RIA firms do not have a dedicated Chief Compliance Officer (CCO) on staff. In our experience in providing compliance support to over 1,400 firms on a monthly basis, we generally do not see RIA firms hire a full-time CCO until the firm reaches in excess of $400 million of assets under management. Firms below that asset threshold, generally have a firm principal that wears the CCO hat and delegates some of the firm’s compliance responsibilities to other staff members. On the other hand, fee-only RIA firms with a single advisor and no staff members, generally have streamlined compliance requirements given that the firm may not have any supervision responsibilities. In addition, investment advisory firm principals have access to compliance software and consulting support to help them successfully and competently fulfill their responsibilities as CCO.

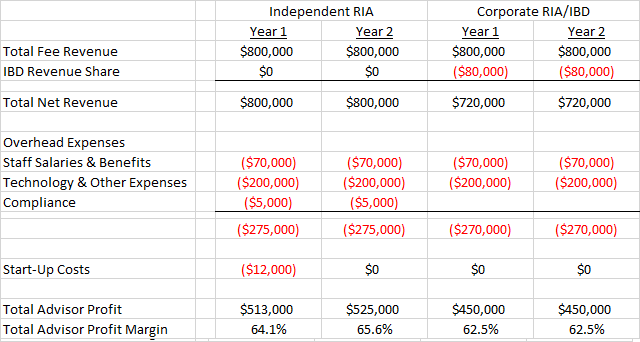

Sample Profit & Loss Statements for an Independent RIA vs. Rep of an Independent Broker Dealer

To illustrate the financial comparisons of operating solely as an independent RIA firm vs. operating as an independent representative, we have broken down three scenarios below for advisors ranging from $40 to $200 million in fee-based assets.

Scenario 1:

- Total advisory assets under management: $40 million

- Number of advisors: 1

- Number of support staff members: 1

In the scenario above, we also make the following assumptions:

- Average advisory fees charged are 1% of total assets under management

- The gross independent broker dealer payout is 85%

- Technology and other overhead expenses such as office rent, insurance, and marketing equate to 30% of gross revenue

- There is a one-time startup cost of $10,000 in year 1 as a new independent RIA firm.

Scenario 2

- Total advisory assets under management: $80 million

- Number of advisors: 2

- Number of support staff members: 1

In the scenario above, we also make the following assumptions:

- Average advisory fees charged are 1% of total assets under management

- The gross independent broker dealer payout is 90%

- Technology and other overhead expenses such as office rent, insurance, and marketing equate to 25% of gross revenue

- There is a one-time startup cost of $12,000 in year 1 as a new independent RIA firm

Scenario 3

- Total advisory assets under management: $200 million

- Number of advisors: 4

- Number of support staff members: 4

In the scenario above, we also make the following assumptions:

- Average advisory fees charged are 1% of total assets under management

- The gross independent broker dealer payout is 92%

- Technology and other overhead expenses such as office rent, insurance, and marketing equate to 15% of gross revenue

- There is a one-time startup cost of $15,000 in year 1 as a new independent RIA firm

In all three scenarios, there is a compelling financial reward to start an independent RIA firm. In scenario 1, the solo advisor has increased his or her annual profit by $55,000 (+37.7%) by year 2 and in scenario 2, the two advisors have increased their shared profits by $75,000 (+16.7%) by year 2. In scenario 3, for the larger practice with four advisors and four support staff members, the four advisors have increased their shared profits by $150,000 (+11.4%) by year 2. While these three scenarios are only examples and do not fully reflect the scenario of every advisor currently affiliated with an independent broker dealer, in our observations we generally see advisors improve their take home pay by 10-40% after transitioning advisory business to the independent RIA model.

Be sure to check back soon for our next post looking at the long-term business enterprise value an advisor can create by becoming fee-only while operating as an independent RIA.

*Source: SEC and state investment adviser firm reports as of June 8, 2016 available on the SEC Investment Adviser Public Disclosure (IAPD) website.