On December 22, 2020, the Securities and Exchange Commission (“SEC”) finalized changes to the Investment Advisers Act of 1940 to adopt a modernized registered investment adviser (“RIA”) marketing rule. The new rule creates a single rule to replace the current Advertising (Rule 206(4)-1) and Cash Solicitation (Rule 206(4)-3) rules. New related amendments to the Books and Records Rule (Rule 204-2) and Form ADV were also finalized. The Form ADV will now require RIA firms to provide additional information related to their marketing practices to assist the facilitation of the SEC’s examination and enforcement capabilities.

Special Note: The new SEC RIA Marketing Rule was officially published in the Federal Register on March 5, 2021. The rule is now scheduled to become effective on May 4, 2021 and has a compliance deadline of November 4, 2022.

In this post, we take a closer look at the finalized Investment Adviser Marketing rule. The full rule release is over 400 pages so this post will serve as a summary of some key highlights.

Which RIA Firms the New Rule Applies to and When it Takes Effect

The new rule becomes effective 60 days from its official publication. However, SEC-registered RIA firms will have 18 months after the rule becomes effective to comply. It’s also important to note that, as of now, this new rule applies to SEC-registered, but not state-registered investment advisers. This may change if individual states adopt their own updated advertising rules in the future.

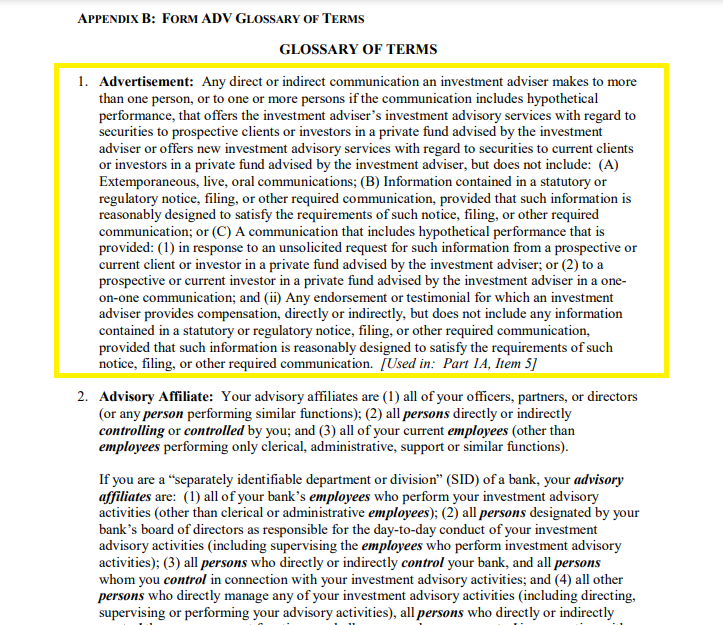

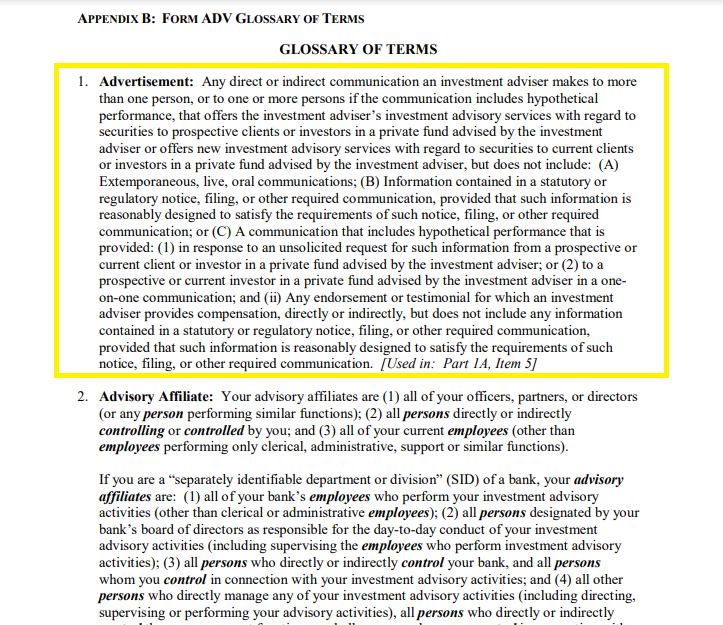

Definition of an Advertisement

According to the final rule summary, the definition of an advertisement was updated in two parts:

- “First, the definition includes any direct or indirect communication an investment adviser makes that: (i) offers the investment adviser’s investment advisory services with regard to securities to prospective clients or private fund investors, or (ii) offers new investment advisory services with regard to securities to current clients or private fund investors. The first prong of the definition excludes most one-on-one communications and contains certain other exclusions.”

- “Second, the definition generally includes any endorsement or testimonial for which an adviser provides cash and non-cash compensation directly or indirectly (e.g., directed brokerage, awards or other prizes, and reduced advisory fees).”

The updated definition of an Advertisement can be found in the updated Form ADV Glossary of Terms:

General Advertisement Prohibitions

According to the new rule, an advertisement may not:

- Include any untrue statement of a material fact, or omit to state a material fact

necessary in order to make the statement made, in the light of the circumstances under which it

was made, not misleading; - Include a material statement of fact that the adviser does not have a reasonable basis

for believing it will be able to substantiate upon demand by the Commission; - Include information that would reasonably be likely to cause an untrue or misleading

implication or inference to be drawn concerning a material fact relating to the investment

adviser; - Discuss any potential benefits to clients or investors connected with or resulting from

the investment adviser’s services or methods of operation without providing fair and balanced

treatment of any material risks or material limitations associated with the potential benefits; - Include a reference to specific investment advice provided by the investment adviser

where such investment advice is not presented in a manner that is fair and balanced; - Include or exclude performance results, or present performance time periods, in a

manner that is not fair and balanced; or - Otherwise be materially misleading.

Uses of Testimonials and Endorsements

The new rule allows for the use of testimonials and endorsements after meeting specific requirements. The rule defines an “endorsement” as “any statement by a person other than a current client or investor in a private fund advised by the investment adviser that:”

- (i) Indicates approval, support, or recommendation of the investment adviser or its supervised persons or describes that person’s experience with the investment adviser or its supervised persons,

- (ii) Directly or indirectly solicits any current or prospective client or investor to be a client of, or an investor in a private fund advised by, the investment adviser; or

- (iii) Refers any current or prospective client or investor to be a client of, or an investor in a private fund advised by, the investment adviser.

On the other hand, the rule defines a “testimonial” as “any statement by a current client or investor in a private fund advised by the investment adviser.”

If an adviser uses testimonials and endorsements in advertisements, they must satisfy specific disclosure, oversight, and disqualification provisions. The final rule summary discusses these requirements in more detail:

- Disclosure: Advertisements must clearly and prominently disclose whether the person giving the testimonial or endorsement (the “promoter”) is a client and whether the promoter is compensated. Additional disclosures are required regarding compensation and conflicts of interest. There are exceptions from the disclosure requirements for SEC-registered broker-dealers under certain circumstances. The rule will eliminate the current rule’s requirement that the adviser obtain from each investor acknowledgements of receipt of the disclosures.

- Oversight and Written Agreement: An adviser that uses testimonials or endorsements in an advertisement must oversee compliance with the marketing rule. An adviser also must enter into a written agreement with promoters, except where the promoter is an affiliate of the adviser or the promoter receives de minimis compensation (i.e., $1,000 or less, or the equivalent value in non-cash compensation, during the preceding twelve months).

- Disqualification: The rule prohibits certain “bad actors” from acting as promoters, subject to exceptions where other disqualification provisions apply.

The rule requires an RIA firm to have a “written agreement with certain persons giving a testimonial or endorsement for compensation above the de minimis threshold.” With regards to the rule, “De minimis compensation means compensation paid to a person for providing a testimonial or endorsement of a total of $1,000 or less (or the equivalent value in non-cash compensation) during the preceding 12 months.”

Use of Third-Party Ratings

Similar to the testimonials and endorsements changes, if an advisory firm provides disclosures and satisfies certain criteria pertaining to the preparation of the rating, the firm can utilize third-party ratings in an advertisement. The rule defines a “Third-party rating” as “a rating or ranking of an investment adviser provided by a person who is not a related person…and such person provides such ratings or rankings in the ordinary course of its business.”

Specifically, the rule states:

- (c) Third-party ratings. An advertisement may not include any third-party rating, unless

the investment adviser:- (1) Has a reasonable basis for believing that any questionnaire or survey used in the

preparation of the third-party rating is structured to make it equally easy for a participant to

provide favorable and unfavorable responses, and is not designed or prepared to produce any

predetermined result; and - (2) Clearly and prominently discloses, or the investment adviser reasonably believes that

the third-party rating clearly and prominently discloses:- (i) The date on which the rating was given and the period of time upon which the rating

was based; - (ii) The identity of the third party that created and tabulated the rating; and

- (iii) If applicable, that compensation has been provided directly or indirectly by the

adviser in connection with obtaining or using the third-party rating.

- (i) The date on which the rating was given and the period of time upon which the rating

- (1) Has a reasonable basis for believing that any questionnaire or survey used in the

Performance Advertising

According to the final rule summary, the following types of performance advertising are generally prohibited with certain exemptions:

- Gross performance results unless the advertisement presents net performance as well

- Any performance results, unless they are provided for specific time periods in most circumstances

- Statements the SEC approved or reviewed any calculation or presentation of performance results.

- Performance results from fewer than all portfolios with substantially similar investment policies, objectives, and strategies as those being offered in the advertisement, with limited exceptions

- Performance results of a subset of investments extracted from a portfolio, unless the advertisement provides, or offers to provide promptly, the performance results of the total portfolio

- Hypothetical performance (which does not include performance generated by interactive analysis tools), unless the adviser adopts and implements policies and procedures reasonably designed to ensure that the performance is relevant to the likely financial situation and investment objectives of the intended audience and the adviser provides certain information underlying the hypothetical performance

- Predecessor performance unless there is appropriate similarity with regard to the personnel and accounts at the predecessor adviser and the personnel and accounts at the advertising adviser. In addition, the advertising adviser must include all relevant disclosures clearly and prominently in the advertisement.

Much of the new rule addresses performance advertising and we will plan to discuss performance advertising in more detail in a future post.

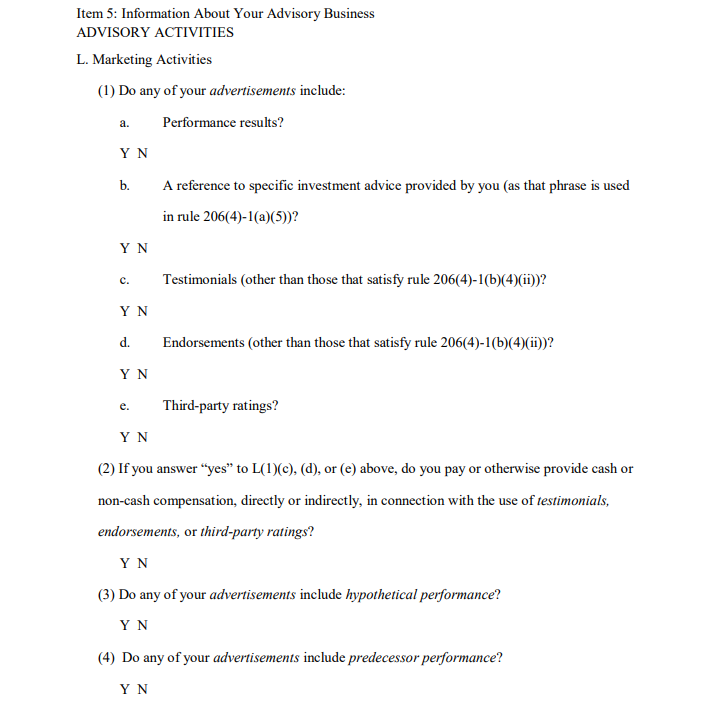

New Form ADV Part 1A Item 5.L

Item 5 of Form ADV Part 1A has been updated to include a new section L. RIA firms will need to disclose if they advertise performance results, use testimonials, use endorsements, or third-party ratings:

With the new Item 5.L, the SEC notes in the rule release “we believe that requiring advisers to address each separately will provide more specific and useful information to our staff regarding whether an adviser engages in these marketing practices.” Furthermore, “Because new subsection L is included under Item 5 of Form

ADV, advisers will be required to update responses to these questions in their annual updating

amendment only.”

Books and Records Rule Updates

There have also been a number of modifications made to the Books and Records Rule to correspond with the new Investment Adviser Marketing Rule. The updates address performance marketing recordkeeping requirements related to predecessor performance and performance marketing more broadly requiring a copy of:

(16) All accounts, books, internal working papers, and any other records or documents that are necessary to form the basis for or demonstrate the calculation of any performance or rate 405 of return of any or all managed accounts, portfolios (as defined in §206(4)-1(e)(11) of this chapter), or securities recommendations presented in any notice, circular, advertisement (as defined in §206(4)-1(e)(1) of this chapter), newspaper article, investment letter, bulletin, or other communication that the investment adviser disseminates, directly or indirectly, to any person (other than persons associated with such investment adviser), including copies of all information provided or offered pursuant to §206(4)-1(d)(6) of this chapter; provided, however, that, with respect to the performance of managed accounts, the retention of all account statements, if they reflect all debits, credits, and other transactions in a client’s or investor’s account for the period of the statement, and all worksheets necessary to demonstrate the calculation of the performance or rate of return of all managed accounts shall be deemed to satisfy the requirements of this paragraph.

Furthermore, there are additional recordkeeping requirements related to the use of testimonials, endorsements, and third-party ratings.

As RIA compliance consultants, we highly recommend that the Chief Compliance Officer (“CCO”) and all advisory firm principals review the SEC’s finalized marketing rule. Investment adviser regulatory compliance issues related to advertising are frequent and the firm’s CCO needs to establish and implement the proper policies and procedures to ensure proper compliance.

Be sure to check back soon as we continue to provide updates on relevant RIA regulatory compliance focus areas.