As part of the SEC’s new Form ADV filing requirements taking effect on October 1, 2017, registered investment adviser (“RIA”) firms will now need to provide more specific information related to regulatory assets under management (“AUM”) and types of clients. The SEC staff notes “we believe several of these new Item 5 questions will require advisers to provide readily available information, such as the number of clients and regulatory assets under management attributable to each category of clients during the last fiscal year.”

Form ADV Changes Taking Effect on October 1, 2017

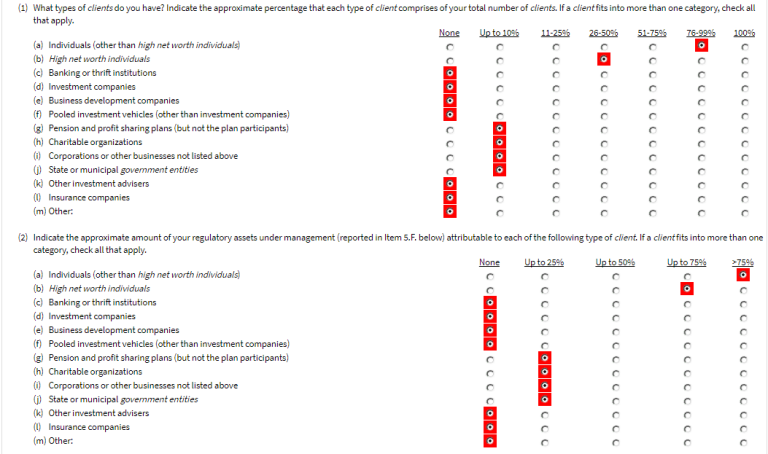

Prior to October 1, 2017, RIA firms have not been required to report the exact number of clients or regulatory AUM by client type. Historically, investment advisers have been able to provide such information by indicating the “approximate percentage” of clients and regulatory AUM by client type:

However, beginning on October 1, 2017, when an RIA firm files a Form ADV amendment, the firm will need to provide more specific information related to the number of clients and associated regulatory assets under management for a given client type. Item 5.D. of the Part 1A will now read as follows:

The Form ADV instructions for Item 5.D. will also now include, “The aggregate amount of regulatory assets under management reported in Item 5.D.(3) should equal the total amount of regulatory assets under management reported in Item 5.F.(2)(c) below.” The SEC staff also noted in the final rule release that, “the categories of clients are the same as those in Item 5.D. of the current Form ADV, except that we are adding ‘sovereign wealth funds and foreign official institutions’ as a client category, and specifying that state or municipal government entities include government pension plans, and that government pension plans should not be counted as pension and profit sharing plans.”

New Form ADV FAQ SEC Staff Guidance

On June 12, 2017, in preparation for the upcoming Form ADV changes, the SEC staff released new Form ADV FAQs related to the new Item 5.D disclosure requirements:

Q: If my advisory firm acts as a subadviser to an investment company, business development company, or pooled investment vehicle, how should I respond to Item 5.D about the category of clients?

A: A firm that subadvises an investment company, business development company, or other pooled investment vehicle is providing advice to such company or vehicle. Accordingly, you should report those assets in Item 5.D. in rows (d), (e) or (f) (as applicable). Do not report the client in Item 5.D.(j) as “Other investment advisers”.

Q: Item 5.D requires advisers to report the approximate number of clients and the amount of total regulatory assets under management attributable to certain categories of client. My advisory firm does not have any high net worth individual clients to report in Item 5.D.(b). Should I check column 5.D.(2) to report “Fewer than 5 Clients” for that category of client?

A: While the staff recognizes that the instructions to Item 5.D. state that “if you have fewer than 5 clients in a particular category (other than (d), (e), and (f)) you may check Item 5.D.(2) rather than respond to Item 5.D.(1), if you do not have any clients for a particular category, the staff encourages you to report “0” in column 5.D.(1), “Number of Client(s)”.

Q: For purposes of Item 5.D, are “pooled investment vehicles” limited to private funds (which are defined in the Form ADV Glossary)?

A: No. For purposes of Item 5.D, pooled investment vehicles include, but are not limited to, private funds. Whether other types of funds (aside from investment companies or business development companies, which are separate categories in Item 5.D.) should be considered pooled investment vehicles depends on the facts and circumstances. The staff believes that, in choosing a category for its client in Item 5.D., an adviser should be consistent with information that it reports internally and in other regulatory filings.

For example, funds that would be investment companies as defined in section 3 of the Investment Company Act of 1940 but for sections 3(c)(5) or 3(c)(11) of that Act would typically be considered pooled investment vehicles in Item 5.D. Similarly, UCITS funds that are regulated by the European Commission and that are not registered under the Investment Company Act would also typically be considered pooled investment vehicles in Item 5.D.

Additionally, the staff believes for purposes of Item 5.D there are some facts and circumstances in which it may be appropriate for an adviser to treat a single-investor fund (also known as a “fund of one”) as a pooled investment vehicle. For example, an adviser could reasonably treat a single-investor fund as a pooled investment vehicle where the fund seeks to raise capital from multiple investors but has only a single, initial investor for a period of time, or where all but one of the investors in the fund have redeemed their interests. However, an adviser generally should not consider a single-investor fund to be a pooled investment vehicle if that entity in fact operates as a means for the adviser to provide individualized investment advice directly to the investor in the fund. See Exemptions for Advisers to Venture Capital Funds, Private Fund Advisers With Less Than $150 Million in Assets Under Management, and Foreign Private Advisers, Investment Adviser Act Release No. 3222 at p. 78-79 (June 22, 2011).

In preparation for the upcoming Form ADV changes, RIA firms need to ensure that portfolio management and reporting systems are modified to properly categorize accounts by client type. In addition, firms should verify that all client accounts are properly classified. Firms will also need to have to readily available reports to calculate the exact number of clients and attributable regulatory AUM organized by client type.