With the strength of the markets over the past few years and frequent reports of registered investment adviser (RIA) record profits and growth, it’s hard to not be excited about the future RIA industry. However, when times are good, it’s also often the best time to begin planning for when times may not be so good. As we all know, markets will turn at some point in the future if they have not already started to turn over these past few days. As such, this second post of our two-part series highlights some areas that principals of investment advisory firms should be looking at when thinking about building an enterprise that can thrive and survive in good and bad market times.

Last week’s post focused on the critical areas of:

- Fixed vs. variable cost structure

- The danger of selling investment performance

- Client concentration risk

This week’s post addresses the final three areas of our six most critical areas that principals should be focused on addressing in order to properly prepare for and survive a market downturn:

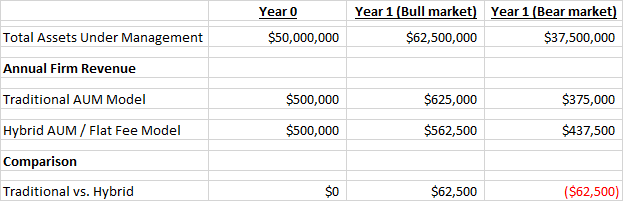

- Understanding the Power and Danger of the AUM Fee Model: As we’ve discussed before, very few industries have the luxury of an established pricing model which has a built-in price escalator as the value of the client’s portfolio, while often volatile, generally rises over time. Vanguard notes that a traditional moderate portfolio (50% stocks and 50% bonds) has an average annual return of 8.4% from 1926-2014. However, the assets under management (AUM) fee model can also lead to a sharp decline in an RIA firm’s revenue without any prior warning. As such, we are seeing an increasing number of successful advisory firms modify the classic 1% AUM fee model by reducing the portfolio management fee to be closer to 50 basis points (bps), or 0.5%, while at the same time introducing a flat annual retainer fee that is equivalent to around 50 bps based on the current value of the client portfolio. On one hand, this hybrid pricing model has less of a built-in price escalator, but on the other hand, it also provides more downside protection to the firm’s revenue during a downturn. Much like an advisor may look to hedge a client’s investment portfolio to mitigate a potential risk, this model allows an advisor to hedge the firm’s revenue stream by trading some potential upside for downside protection. Given that we generally see that advisory firms carry far too high a percentage of fixed costs, downside revenue protection can be quite valuable.

- Our Recommendation: While by no means do we advocate that RIA firms abandon the compelling AUM-based pricing model, firms may want to consider “de-risking” the pricing structure by coupling AUM-based pricing with flat retainer fees tied to holistic services such as financial planning.

This simplified chart further illustrates the trade-offs between the AUM and hybrid (AUM and flat fee) pricing models in a bull and bear market:

- The Risk of Just Providing Portfolio Management: Two questions that serve as a good barometer for this risk are 1) what materials are being presented to clients during a regular meeting? and 2) what percentage of the meeting is being spent discussing the client’s investment portfolio? If the RIA firm is not providing a personal balance sheet to clients and more than 25% of the meeting is being spent discussing the client’s investment returns, it’s likely that the advisory firm’s relationships with its clients are not as deep or as valuable to the client as they could be. A personal balance sheet allows theadvisor to focus the conversation not just on the investment portfolio, but rather on the much larger personal financial picture. It also is a great conversation starter often revealing areas of opportunity for theadvisor to add additional value and even perhaps increase asset wallet share. In our experience, portfolio management is the most difficult way for an advisory firm to differentiate itself and should never be the key driver of attracting or retaining clients.

- Our Recommendation: Move quickly to offer additional services such as financial, estate, and tax planning or other family office-like services such as managing household staff or bill pay, to clients that add substantive value and are at less of risk being replaced during market downturns when financial belts tighten.

- Preparing for Increased Regulatory and Legal Risks: In our experience as RIA compliance consultants, client complaint volume is generally strongly inversely correlated to market performance. In other words, during and following a market downturn, the number of investor complaints spikes. Whether legitimate or not, such complaints pose a tremendous risk to advisory firms of all sizes given the potential financial costs. It’s critical that the proper compliance policies and procedures have been implemented to produce detailed documentation that will be invaluable in handling any client disputes. Furthermore, be sure to increase client communication during times of market volatility to ensure clients are informed and to also review client suitability information to confirm that clients’ investment strategies match their documented risk tolerances. When markets take a turn for the worst, it’s vital that the RIA firm has the proper budget and capital available to increase its compliance resources.

- Our Recommendation: Make sure to properly allocate for potential increased regulatory and legal fees given the increased risk of problems or client complaints following a market downturn.

Be sure to check back soon as we further discuss opportunities for principals of investment advisory firms to strengthen operations and enhance the performance of their firms.