This is a guest post from Bonnie Treichel, J.D., Senior Consultant & Chief Compliance Officer at Multnomah Group, Inc.

You know the new rules, but how do you get everyone at the firm to comply? Isn’t this the challenge for every compliance officer? It’s easy to theorize about rules and regulations, policies and procedures, training advisers, and creating a culture of compliance, but where the rubber meets the road is inside a registered investment adviser (“RIA”) firm implementing new rules on the ground floor – and it’s not always easy. This post will explore the steps our firm takes once a new rule or regulation is implemented – from understanding the rule to ongoing monitoring of staff – and what it takes to remain compliant in an ever-changing financial services marketplace.

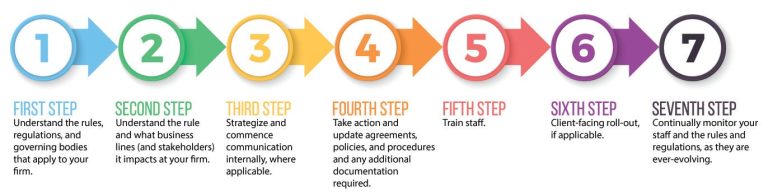

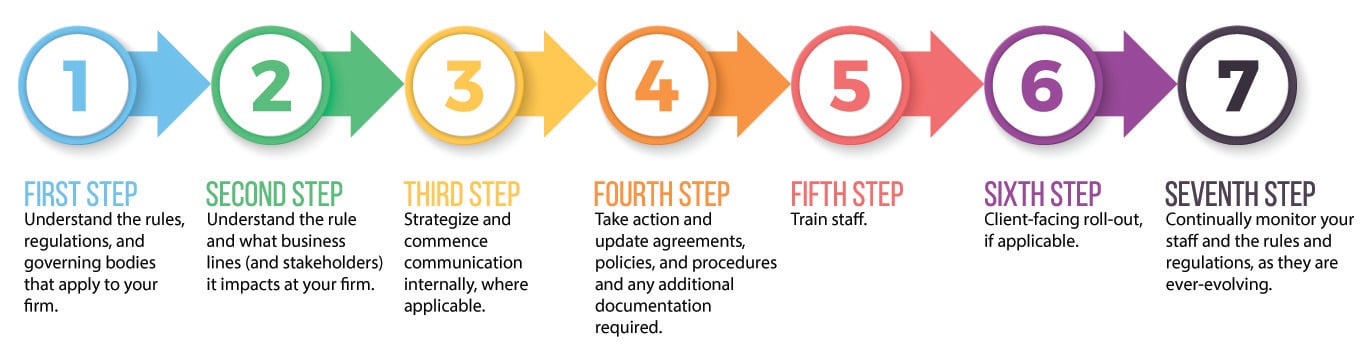

Step 1: Understand the rules, regulations, and governing bodies that apply to your firm.

Start by understanding the rules and regulations – as well as governing bodies – that apply to your firm. For example, is the firm an SEC-registered firm or a state-registered firm? If the firm is state-registered, these advisers are governed primarily by state law (although many state law provisions are taken from the Investment Advisers Act of 1940 and the SEC Rules).

Using the example of the Department of Labor’s (“DOL”) fiduciary rule, many advisers were not concerned with the DOL nor the Employee Retirement Income Security Act (“ERISA”) until April 2015 when the DOL re-proposed the fiduciary rule and expanded the scope to include IRAs. Advisers who traditionally had no need to pay attention to ERISA suddenly had cause to take note and comply.

One way to better understand which rules and governing bodies apply to your firm is to use a third-party tool or resource that can assist your firm in staying up-to-date with all sources of law and regulation that may impact your firm. Our firm work with a third party to receive updates to ensure we continually stay abreast of new and changing rules, including the new DOL fiduciary rule.

Step 2: Understand the rule and what business lines (and stakeholders) it impacts at your firm.

Once you receive notice that a new rule or regulation applies to you, review the rule to understand how it applies to you (and how it applies to your competition). In some cases, you may need to call upon outside counsel or a third-party resource for assistance.

Going back to the fiduciary rule, this rule had widespread impact on the business lines and stakeholders at most firms. Many new rules either impact the high net worth business or the retirement plan business, but the fiduciary rule impacted both business lines for many firms.

By first classifying the business lines that were impacted, our firm could identify the stakeholders that should be involved in early conversations to drive the business strategy. Keep in mind that a compliance conversation is more than just compliance – it’s a business discussion and often impacts business development, marketing, compliance, legal, product development, and operations.

Step 3: Strategize and commence communication internally, where applicable.

Start scheduling meetings with key stakeholders to review the impact of the rule from your perspective and gain an understanding of how the other stakeholders at your firm believe such new rules may be impacting them. For example, schedule meetings between compliance and marketing to discuss how a rule might be conveyed to clients, if necessary. In addition, start scheduling meetings between compliance and operations to discuss whether any new workflows will be required to support the new rule or regulation.

Consider creating a timeline leading up to the compliance date for the rule, which includes the key dates for communicating to staff, updating policies and procedures, training staff, and communicating to clients (if applicable). In creating a timeline, work backward from the compliance date and leave plenty of extra time. Remember, it’s never too early to start the discussion with key personnel as communication is critical to bringing the firm up-to-speed with changing regulations.

Step 4: Take action and update agreements, policies, and procedures and any additional documentation required.

Before updating documentation, take inventory of all documents that require changes and the way in which these documents will impact one another. Once the firm has an inventory of documents that require updates, commence with the incorporation of the new rule into your documents, which may include:

- Policies and procedures

- Agreements

- Staff training

- Client-facing forms and disclosures

Leave extra time for this phase as key stakeholders will need to review these documents and often changes to one document impact several other documents.

Step 5: Train staff.

Training staff is the most critical step, and often one of the least valued. At our firm, staff training is not limited to one 30-minute WebEx; staff training is an ongoing process through several different channels. Examples of staff training and communication include:

- Communicate to staff via an intranet or internal chat feature. Our firm uses the “Chatter” function of Salesforce to communicate in a newsfeed any key information such as new clients, internal meetings, changes to firm policies, upcoming office closures. Introducing the changes to a new rule via a newsfeed will give staff an idea of what’s to come.

- Schedule a series of training sessions and incorporate case studies into the training. The old PowerPoint routine becomes stale (though we certainly still used a ton of PowerPoint at our firm), so consider ways to train your staff that doesn’t focus solely on one bullet point after another. One way to engage staff is through the use of case studies and hypothetical scenarios that test the knowledge developed in the training session.

- Utilize follow-up emails to remind staff about the new policies learned and implemented during prior meetings; consider a quick reminder with short bullet points and encourage staff to ask questions if they need additional information. In a constantly-evolving financial services industry, it is critical to remind staff what they learned.

And, consider the following additional tips for your training:

- Find a sales opportunity for advisers, where possible. In general, advisers don’t want to waste valuable time that could be spent on prospecting new clients and servicing existing clients to learn about rules and regulations. If there is an opportunity to make a rule or new policy into a sales differentiator, advisers will be more apt to embrace regulatory training.

- Segregate staff and advisers, where necessary. In some cases, the entire firm needs to be a part of the training, but in other cases, support staff may require a truncated version of what should be a more in-depth version for advisers. Consider crafting training sessions that meet the needs of the various groups of staff at your firm.

- It should go without saying, but avoid introduction of policies around a new rule or regulation at the end of the three-day company meeting marathon. Likewise, avoid training sessions after lunch.

Step 6: Client-facing roll-out, if applicable.

Prepare staff to introduce new rules to clients, where appropriate. Some new policies may not require an introduction to clients, but other new rules that precipitate changes for clients, such as the DOL fiduciary rule or Money Market Reform, may require a roll-out strategy that begins internally and extends to clients. While you don’t want to communicate too early before you have a coherent plan, you don’t want your client to hear about a new rule from a competitor.

Step 7: Continually monitor your staff and the rules and regulations, as they are ever-evolving.

Once you roll-out new rules to staff and clients, the role of the compliance officer is not over, but is just beginning. New rules require ongoing monitoring to ensure that staff continually follow the newly-adopted policies and procedures. Further, the new policies require monitoring, as tweaks may be required over time. For example, if you implemented a new client form because of the rule – such as the fiduciary rule where many due diligence forms have been implemented to support IRAs – then over time, I suspect many firms may make small improvements to their forms.

Additionally, the rules are constantly changing and as such, require continual monitoring. As mentioned above, if continually monitoring poses a challenge for your firm, hire a third party to assist with the ongoing monitoring of rules and regulations to keep your firm apprised of what is changing and how it applies to you.

Now it’s time to get to work communicating to your staff about all of your recently-updated policies and procedures as a result of the new rules out there because, as we all know, there’s not a shortage of changing rules and regulations!

About this Guest Author: Bonnie Treichel

Bonnie M. Treichel is a Senior Consultant for Multnomah Group. She is also a member of the firm’s Technical Services Committee and serves as the Chief Compliance Officer. Bonnie promotes a culture of compliance at Multnomah Group, offering expertise on a variety of ERISA and retirement plan-related issues.

Prior to joining Multnomah Group, Bonnie was a partner at a law firm that specialized in all aspects of retirement-related products and services – working both with plan sponsors and retirement plan service providers. Bonnie has been a frequent speaker on the topic of retirement plan issues at local, regional, and national conferences and events.

Bonnie earned her J.D. from Pepperdine University School of Law, where she graduated with honors and received a certificate from the Palmer Center for Entrepreneurship & the Law. She also graduated with honors from Truman State University, in Kirksville, Missouri, earning a degree in Political Science. Bonnie is a member of the State Bar of California.

Note: The information contained herein is provided by a third party not affiliated with RIA in a Box LLC. It is not intended to be a comprehensive analysis or apply to any one investment adviser’s particular situation and may not reflect the views of RIA in a Box LLC.